Loan up to 10 Core * | Tenure 36-180 Months | Interest Rate Starting at 9.5%* p.a.

A Loan Against Property (LAP) is a secured loan that lets individuals or businesses borrow against the value of their residential or commercial property to fulfill their financial needs, whether for business expansion, personal reasons, education, or medical expenses. LAP is available to salaried individuals, self-employed individuals, and SMEs alike in a flexible tenure, with favorable interest rates and high loan amounts.

In most cases, lenders will offer up to 60% of the property‘s market price for residential properties, and up to 70% for commercial properties. This means that if your residential property is valued at ₹50 lakhs then you can get a loan for ₹30 lakhs; and if it‘s a commercial property, you can get one up to ₹35 lakhs. The amount of the loan sanctioned will depend on several key factors for eligibility.

Lenders evaluate your eligibility based on various factors such as income level, age, employment type, ownership of the property, credit score, valid documentation, and others. In addition to the value of the property, your capacity for repayment is very important. Your capacity to repay is assessed based on your monthly income, current liabilities, type of business/job, and history of repayment.

Knowing the eligibility criteria is very important step to a smooth and successful loan application. Read on to learn about the full eligibility norms and prepare yourself to raise the chances of being approved.

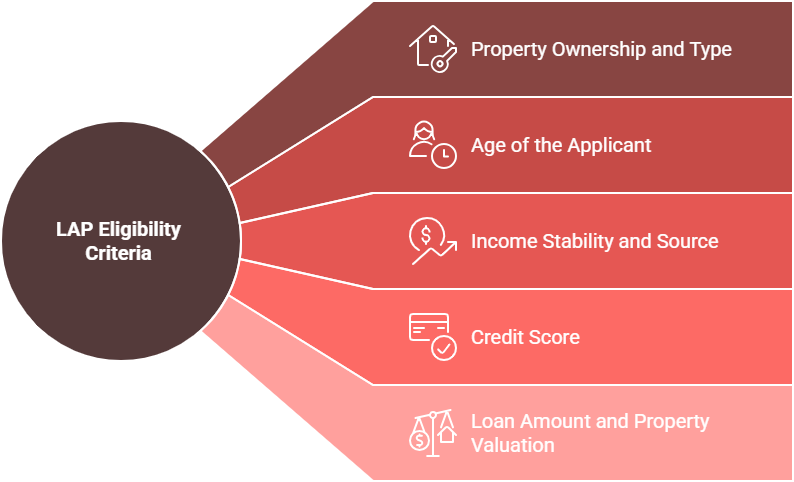

| Criteria | Salaried Individuals | Self-Employed Individuals | SMEs |

| Property Ownership and Type | Must own a clear-title residential or commercial property. | Must own a clear-title residential, commercial or industrial property. | Business or promoter must own the property in firm/partner's name. |

| Age of the Applicant | Must be an Indian. 21 – 60 years (at loan maturity) | Must be an Indian. 25 – 65 years (at loan maturity) | Must be Indian SME. At least two years old. |

| Income Stability and Source | Minimum 2–3 years of continuous employment with regular salary. | Minimum 3 years in current business with audited financials. | Minimum 2-3 years of stable business operations with turnover proof. |

| Credit Score | 700 and above preferred for best terms. | 700 and above preferred; lower score may reduce eligible amount. | 700 and above preferred; credit history of firm and promoter matter. |

| Loan Amount & Property Valuation | Up to 60% of residential & 70% of commercial property value. | Same as salaried; subject to proper valuation and income proof. | Up to 70% of business premises or collateral value; flexible structure possible. |

When applying for a Loan Against Property, you will have to submit some base documents to enable your lender to verify your identity, income and Property details. The documents are essential, as they help verify your eligibility for the loan with the bank, while expediting the loan process.

Documents differ slightly for salaried, self-employed, and business applicants. Notably, all applicants have the basic proofs such as identification, address verification, income proof, and property documents. Having all papers completed and accurate will greatly improve the speed of the process and offer better and faster loan products.

| Types | Salaried Individuals | Self-Employed Individuals | SMEs |

| Identity Documents | PAN Card/Aadhaar Card/Driving License/Voter ID/Passport | PAN Card/Aadhaar Card/Driving License/Voter ID/Passport | GST Registration Certificate (if applicable) and Other Applicable Registrations, KYC of Partners/ PAN Card/Aadhaar Card/Driving License/Voter ID/Passport |

| Address Proof |

• Electricity bill for owned premises • Rent agreement for rented premises • Passport |

• Electricity bill for owned premises • Rent agreement for rented premises • Passport |

• Electricity bill for owned premises • Rent agreement for rented premises • Udyam Certificate/GST Registration Certificate |

| Income Documents | • Minimum 3-month salary slips. |

• Income Tax Returns, along with computation for the last 2 years • Profit/Loss statement and balance sheet for the last 2 years, GST Returns |

• Income Tax Returns, along with computation for the last 2 years • Profit/Loss statement and balance sheet for the last 2 years, GST Returns |

| Bank Account Statement | Salary credit bank account statement for the last 6 months | Operative bank account statement for the last 12 months | Operative bank account statement for the last 12 months |

| Property Documents | Relevant documents of property given as collateral | Relevant documents of property given as collateral | Relevant documents of property given as collateral |

A mortgage loan or loan against residential property is a secured loan in which you use your residential or commercial property as a security. It is a secured form of loan where you can avail a large amount in the form of loan which can be paid in equal installments of amount that one can easily afford in a given period.

This type of secured loan is most appropriate if an individual is in dire need of a large amount of money for some essential purposes. Some common reasons to borrow include:

Yes, you can get a loan against commercial property. To apply for one, follow the below steps:

On successful verification, the loan amount will be disbursed into your bank account instantly.